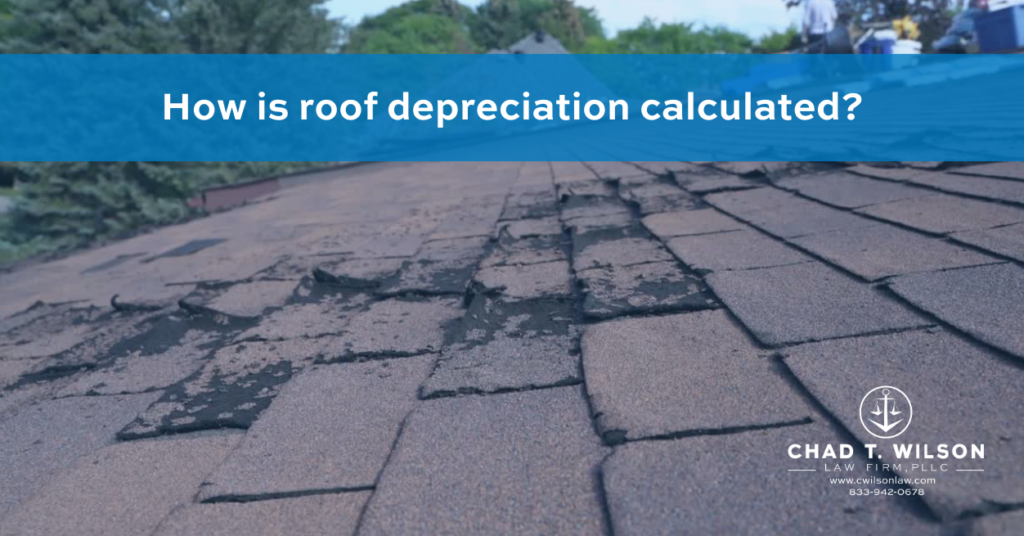

How is roof depreciation calculated?

Insurance companies frequently use different components to determine a roof’s depreciation. The procedure entails determining the roof’s age, estimated lifespan, and degree of wear and tear.

It is simple to determine depreciation depending on age. Assume your roof has a 20-year lifespan and is five years old when it becomes damaged. Yearly, a roof loses around 5-20% of its worth.

When examining a roof, a claims adjuster will take its age and condition into account. There might be little to no adjustment for the condition if the roof is in respectable condition for its age. The adjuster may, however, increase the depreciation estimate if the roof is in bad condition, has received insufficient repairs, or has been the subject of earlier claims.

What Depreciation Means for Your Roof Insurance Claim.

As your house gets older and wears out, its value may decrease. Depreciation is a term used in finance to describe this loss of value. You need to be aware of how depreciation affects the claim procedure if a storm damages the roof of your home.

It’s vital to remember that insurance companies may use various methods to determine the depreciation of roofs. The precise calculation procedures can change depending on the insurer, the conditions of the insurance, and regional laws.

To understand how depreciation is computed in their specific scenario, policyholders should check their insurance policy and speak with their insurance agent or adjuster.

Insurance companies make an estimation of the depreciation value by taking into account the age of the roof, anticipated lifespan, wear and tear, and upkeep. To make sure that homeowners repair their roof to its pre-loss condition while accounting for its current value, this aids in determining the amount withheld and then issued as a depreciation check.

Here is an explanation of how insurance companies often determine a roof’s depreciation:

Age

The age of the roof affects its depreciation considerably. The age of the roof at the time of the claim is taken into account by insurance carriers. Older roofs have a higher likelihood of having noticeable signs of wear and tear, which can lower their value and increase the depreciation rate. The installation date or the homeowner’s information helps calculate the age.

Maintenance

Maintenance and upkeep affect the roof’s depreciation. The homeowner’s efforts to maintain the roof, such as routine inspections, repairs, and cleaning, may be taken into account by insurance carriers. The lifespan of the roof can be increased, and depreciation can be reduced, with proper maintenance.

Wear and tear

Exposure to different elements, such as sunlight, rain, wind, and temperature changes, can cause wear and tear on the roof. To evaluate the roof’s condition and spot wear and tear indicators like curled or broken shingles, missing granules, or sagging sections, insurance adjusters inspect it. The depreciation estimate takes into account the degree of wear and tear.

Lifespan

Insurance firms also take into account the anticipated lifetime of the roofing material. The lifespans of various roofing materials vary. For instance, metal roofs can last 40–70 years, whereas asphalt shingles normally only last 20–30 years. The amount of depreciation is calculated by the insurance provider using the predicted lifespan as a percentage of the actual lifespan.

Insurance firms compute depreciation using a variety of estimating techniques. Some people may rely on depreciation charts that are considered industry standards and that determine the amount of depreciation based on the age of the roof. Others may use computer systems or internal estimators that take criteria into account while calculating the depreciation value.

Actual Cash Value

The claim’s cash value (ACV) is often determined to include the roof’s depreciation. The ACV is the depreciation-adjusted value of the damaged goods at the time of the loss. The insurance provider deducts the depreciation amount from the roof’s replacement cost value (RCV) to get the ACV.

If your roof is ever damaged, give The Chad T. Wilson Law Firm a call right away. We are here to assist you if your insurance claim is being denied or underpaid.

Is your claim being denied or underpaid? Call Chad T. Wilson Law Firm, PLLC.

Speak with one of our attorney if you’re having trouble getting your claim processed or if the insurance company is attempting to pay less for the claim than is reasonable.

Contact us: https://cwilsonlaw.com/contact-us/

Learn more about our attorneys:

https://cwilsonlaw.com/meet-the-team-chad-t-wilson-law-firm-pllc-insurance-attorney/

Follow us on Social media:

https://beacons.ai/chadtwilsonlaw