Chad T. Wilson – News

August 2, 2023

Updated: August 2, 2023

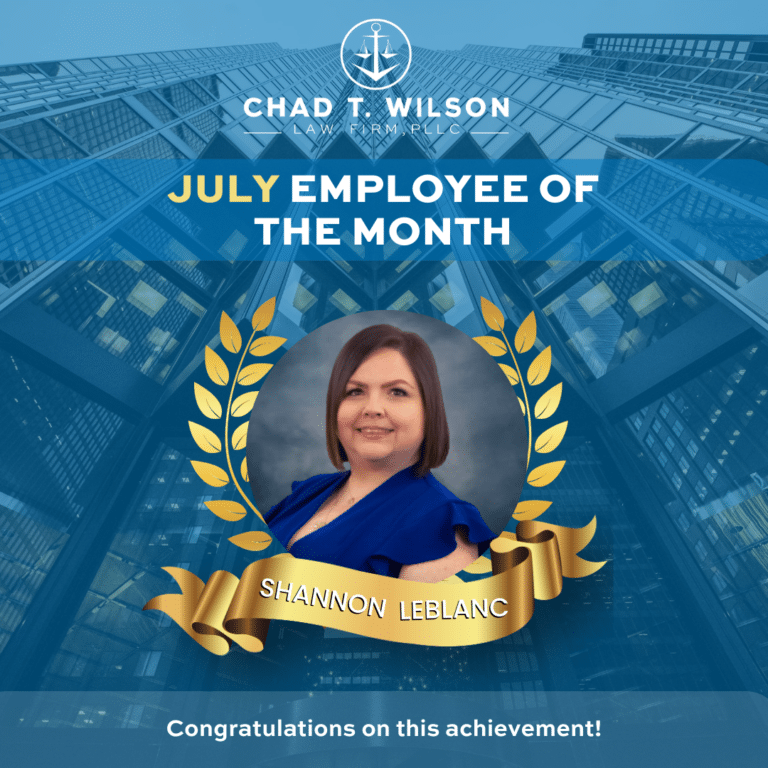

Chad T. Wilson: July, 2023 Employee of the Month!

Meet Shannon, our most recent employee of the month candidate!

Shannon began her career in accounting in 2013 within the oil and gas industry, where she quickly advanced and cultivated her passion for numbers. She also holds over 20 years of customer service and office administration experience. She made the move into legal and trust accounting in 2017, when she joined Chad T. Wilson Law Firm. Shannon currently manages all settled cases for the firm, along with various other accounting and administrative aspects.

In her free time, she loves spending time with her family. Shannon has three children and two grandchildren who keep her busy. She also enjoys traveling, cooking, reading, and art.

When other candidates were asked why they nominated Shannon July’s Employee of the Month, one said:

“Shannon goes above and beyond every day. She is my go-to for a second opinion and is always thinking ahead. She is not only very smart, but also wonderful to work with.”

Congratulations on this wonderful achievement Shannon.

Learn more about our team at:

https://cwilsonlaw.com/meet-the-team-chad-t-wilson-law-firm-pllc-insurance-attorney/

Contact our Chad T. Wilson Law Firm Office Locations to Schedule a free Consultation.

Chad T. Wilson is an attorney whose firm specializes in property insurance disputes.

Written By:

Alejandro Caro